Every business reaches a point where growth demands capital. Whether it is hiring, expanding operations, investing in technology, or simply managing cash flow, funding decisions shape not just how a business grows, but how fast and how sustainably.

At the heart of this decision lies a common debate: bootstrapping vs business loan.

On the surface, it looks simple. Bootstrapping means using your own money. A loan means borrowing from someone else. But the real difference goes much deeper. It is about control, risk, speed, and most importantly, the cost of capital.

This blog breaks down the true cost behind both choices so businesses can make informed, practical decisions.

What is Bootstrapping in Business Finance?

Bootstrapping refers to building and running a business using personal savings, internal revenue, or minimal external support.

In this approach, the business relies entirely on its own resources. There are no lenders involved and no fixed repayment obligations. Expenses are managed through existing cash or reinvested profits.

For many founders, this offers a strong sense of independence. Decisions remain internal, without pressure from external stakeholders.

However, this independence comes with a cost that is not always immediately visible.

What is an Unsecured Business Loan?

An unsecured business loan is a form of borrowing that does not require collateral. Instead, lenders evaluate factors such as creditworthiness, business performance, and repayment capacity.

These loans are typically used for managing working capital, expanding operations, investing in marketing, or purchasing equipment.

They are relatively quick to access, especially for businesses that may not have assets to pledge. However, this convenience comes with trade-offs.

Unsecured loans generally carry higher interest rates compared to secured options, along with shorter repayment timelines and stricter eligibility requirements.

This is where the concept of cost of capital becomes important.

Understanding the Cost of Capital

The cost of capital is the price a business pays to access funds.

In the case of a loan, this is visible as interest and repayment obligations. In the case of bootstrapping, it shows up in less obvious ways.

It can include:

- Interest paid on borrowed funds

- Opportunity cost of using personal capital

- The return the business needs to generate to justify the funding

- The strain placed on cash flow due to funding decisions

Both bootstrapping and borrowing involve costs. The difference lies in how those costs appear.

With loans, the cost is explicit and measurable. With bootstrapping, it is often indirect and easier to overlook.

The True Cost of Bootstrapping

Bootstrapping is often seen as the safer route because there is no debt involved. In reality, the cost is simply structured differently.

1. Opportunity cost of personal capital

When you invest your own savings into a business, you give up alternative uses of that money.

That capital could have been invested elsewhere, kept aside for financial security, or allocated to lower-risk opportunities. While this does not appear in financial statements, it is still a real cost that affects long-term financial decisions.

2. Slower startup growth financing

Bootstrapped businesses rely on internal cash flow to grow, which naturally limits the pace of expansion.

Constraints in capital often affect hiring, marketing, and product development. For instance, a business may delay scaling its marketing efforts or expanding its team simply because funds are not immediately available.

In competitive markets, timing plays a critical role. Slower execution can result in missed opportunities that are difficult to recover later.

3. Higher personal risk

Bootstrapping shifts the financial risk directly onto the founder.

If the business faces a downturn, the impact is not limited to operations. Personal savings and financial stability are also at stake, with little separation between business and personal exposure.

4. Cash flow pressure

Without external funding, day-to-day operations depend entirely on incoming revenue.

This becomes challenging when there are delays in receivables or unexpected expenses. Fixed costs such as salaries, rent, and vendor payments continue regardless of when cash comes in, creating constant pressure on liquidity.

5. Limited scalability

Bootstrapped businesses often prioritize steady growth over rapid expansion.

While this approach can create a stable foundation, it may limit the ability to scale quickly. Entering new markets, investing in innovation, or strengthening competitive positioning often requires upfront capital.

In industries where scale drives advantage, this can become a meaningful constraint.

The True Cost of an Unsecured Business Loan

Loans make capital available quickly. But they introduce financial obligations that need to be managed carefully.

1. Interest as a direct cost of capital

The most visible cost of an unsecured business loan is interest.

Since these loans are not backed by collateral, interest rates are typically higher than secured options and vary based on the business’s credit profile, financials, and lender assessment. This directly increases the overall cost of borrowing.

2. Fixed repayment obligations

Loans come with structured repayment schedules that must be followed regardless of business performance.

This can put pressure on cash flow, especially when there are delays in receivables or fluctuations in revenue. It also reduces flexibility in how working capital is managed.

3. Shorter repayment cycles

Unsecured loans generally have shorter repayment tenures compared to secured funding.

As a result, monthly outflows tend to be higher, which can strain businesses that are still stabilizing their cash flows.

4. Qualification barriers

Not all businesses can access unsecured loans easily.

Lenders typically look for stable revenue, a strong credit profile, and consistent financial records. This makes it more challenging for early-stage businesses without a track record to qualify.

5. Financial discipline requirement

Borrowed capital brings a level of accountability.

Businesses need to plan cash flows carefully, prioritize spending, and ensure that the funds are used in a way that generates returns. While this improves financial discipline, it also limits flexibility in the short term.

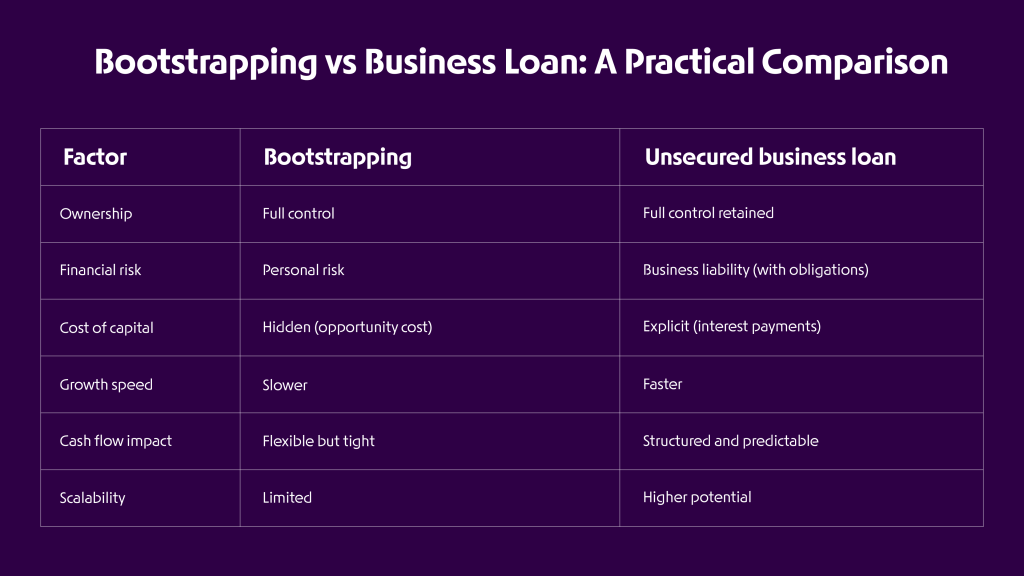

Bootstrapping vs Business Loan: A Practical Comparison

When comparing bootstrapping vs business loans, the decision is less about which is better and more about which cost structure aligns with your business.

When Bootstrapping Makes More Sense

Bootstrapping works well when:

- The business has low initial capital requirements

- Growth can be gradual and supported by internal cash flow

- Founders want to retain full control over financial and operational decisions

- Revenue generation begins early in the business lifecycle

It is especially suitable for service-based businesses or niche markets where scaling does not require significant upfront investment.

When an Unsecured Business Loan is the Better Choice

An unsecured business loan is more suitable when:

- The business has predictable cash flows

- There is a clear and actionable growth opportunity

- Speed of execution matters

- The expected return on investment exceeds the cost of capital

In such cases, borrowing can support faster expansion and improve overall business value. Solutions like OPEN Capital’s unsecured business loans are designed to enable quick access to funds with minimal documentation, helping businesses act on opportunities without delay.

The Hidden Trade-Off: Speed vs Cost

The decision in bootstrapping vs business loan ultimately comes down to a trade-off between speed and cost.

Bootstrapping keeps financial obligations low but often slows down growth. Borrowing increases the cost of capital, but allows businesses to move faster and act on opportunities sooner.

A slower business may save on interest but risk losing market share. A faster-growing business may incur higher borrowing costs but capture opportunities early.

Both approaches involve trade-offs. The difference lies in when and how those costs are incurred.

A Balanced Approach to Startup Growth Financing

In practice, many businesses do not rely entirely on one approach.

They often begin with bootstrapping and gradually introduce external funding as the business stabilizes and grows.

This hybrid approach allows businesses to:

- Maintain control in the early stages

- Validate their business model before taking on financial obligations

- Use loans strategically to support expansion and growth opportunities

It combines the discipline of bootstrapping with the scalability of external funding.

Conclusion

There is no universal answer to the bootstrapping vs business loan debate.

Bootstrapping offers independence but can limit the speed of growth. An unsecured business loan provides access to capital but comes with financial obligations that need to be managed carefully.

The right choice depends on:

- The stage of the business

- Industry dynamics

- Risk appetite

- Growth goals

Understanding the cost of capital in both scenarios is essential.

In the end, funding is not just about accessing money. It is about deciding how your business grows, how fast it scales, and the level of risk you are willing to take along the way.

If you are exploring funding options, OPEN Capital’s unsecured business loans can help you access the capital you need to move forward, without the need for collateral.

FAQs

- What is bootstrapping in business finance?

Bootstrapping is the process of starting and growing a business using personal savings or internal revenue, without relying on external funding. - Is an unsecured business loan risky?

An unsecured business loan carries risk due to higher interest rates and fixed repayment obligations. However, when used carefully, it can also support growth without requiring collateral. - What is the cost of capital in simple terms?

The cost of capital is the price a business pays to access funds, including interest, opportunity cost, and the returns expected from using that capital. - Can startups combine bootstrapping and loans?

Yes, many businesses begin by bootstrapping and later introduce loans to support expansion once they have more stable cash flows.