A small manufacturing business applies for a working capital loan. Its monthly sales are stable, GST returns are filed regularly, and the company receives payments from long-standing clients every month. Yet the loan application gets delayed because the business has little formal borrowing history and a limited credit record.

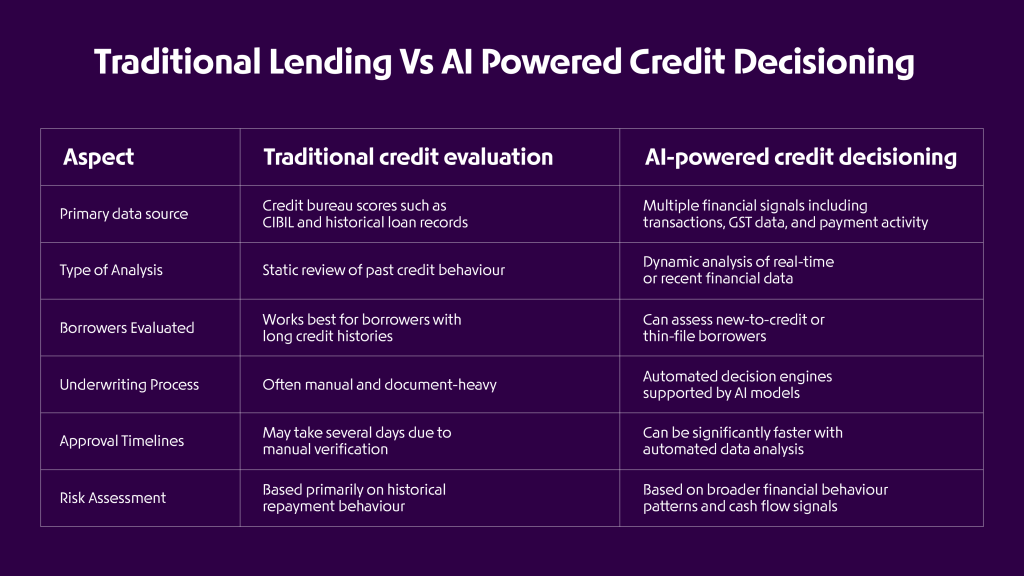

Situations like this are common for many small and medium enterprises. Traditional lending systems often rely heavily on credit bureau scores to evaluate borrowers. When a business does not have an extensive credit history, lenders may struggle to assess its risk accurately.

This is where AI credit decisioning in India is beginning to reshape how lending works. By analysing financial signals such as bank transactions, GST filings, and revenue patterns, lenders can evaluate businesses more holistically and, in some cases, approve a business loan without a CIBIL score, especially when other indicators of financial stability are strong.

The Limits of Traditional Credit Scores

Credit bureau scores such as CIBIL primarily reflect a borrower’s past repayment behaviour based on their credit history. They work well when a borrower has an established record with multiple loans or credit cards.

However, this model has clear limitations when applied to small businesses. Many SMEs operate successfully for years without taking formal credit. When they finally apply for a loan, they often have a “thin” or non-existent credit profile.

Traditional underwriting processes also rely on documentation such as:

- Historical financial statements

- Income tax returns

- Collateral assets for certain loan types

- Bank statements for financial verification

For many growing businesses, these requirements can slow down the loan evaluation process. Even with detailed documentation, traditional models may not always capture the day-to-day financial activity of a business.

As a result, some viable SMEs find it difficult to qualify for formal credit using conventional scoring frameworks alone.

What Is AI Credit Decisioning?

AI credit decisioning refers to the use of artificial intelligence and machine learning to improve how lenders evaluate loan applications. Instead of relying only on traditional credit scores, these systems analyse large datasets that include alternative financial signals such as transaction history, utility payments, and cash flow patterns.

This approach helps lenders assess borrowers more accurately and approve loans faster, even when a borrower has limited credit history.

Key capabilities of AI credit decisioning include:

- Broader data analysis: AI can evaluate alternative financial data, helping lenders assess borrowers with thin or limited credit histories and strengthening alternative credit scoring in India models.

- Faster loan approvals: Automated decision engines can review borrower data within minutes, reducing approval timelines that previously took days.

- Improved risk management: Machine learning models analyse financial behaviour patterns to identify potential risk signals earlier in the credit evaluation process.

- Consistent decisioning: Automated systems apply the same evaluation rules across applications, reducing subjective decision-making and ensuring consistent underwriting.

By combining multiple financial signals, AI-powered systems enable lenders to make faster and more reliable credit decisions.

The Rise of AI Credit Decisioning

AI-driven credit models are designed to evaluate borrowers using a much broader set of financial data. Instead of focusing only on historical loan behavior, these systems analyse multiple indicators that reflect the real performance of a business.

Modern credit decisioning platforms are capable of processing large volumes of structured and unstructured financial data in seconds. These systems analyse patterns in revenue stability, payment behaviour, transaction flows, and compliance records.

By automating this analysis, lenders can reduce the time required for underwriting while maintaining consistent risk evaluation. Automated underwriting systems also reduce manual data entry and allow lenders to process large volumes of loan applications efficiently.

This approach is often referred to as AI underwriting SME, where technology assists credit teams in identifying reliable borrowers more quickly.

Alternative Credit Scoring: Looking Beyond Bureau Data

One of the key developments in digital lending is the emergence of alternative credit scoring India. Instead of relying solely on bureau scores, lenders now evaluate a variety of financial and operational signals.

These may include:

- Bank transaction history

- Digital payment activity

- Utility and telecom bill payments

- Invoice and receivable patterns

- Tax filings and compliance records

Such alternative data sources provide a deeper understanding of a borrower’s financial behaviour. AI models can analyse these signals continuously, identifying trends that traditional systems may overlook.

For example, consistent inflows in a bank account, regular supplier payments, and steady revenue patterns can indicate financial stability even when a borrower lacks a strong credit history.

This broader view of financial behaviour is enabling lenders to evaluate borrowers who were previously considered “new-to-credit”.

The Role of GST Data in Credit Assessment

One of the most powerful data sources for business lending today is GST filings. With millions of businesses submitting regular returns, GST data provides reported insights into revenue patterns, tax compliance, and trading relationships.

This has led to the emergence of GST-based lending, where lenders use GST filings to assess the financial performance of a business.

GST data allows lenders to analyse:

- Monthly revenue trends

- Purchase and sales patterns

- Buyer and supplier networks

- Filing discipline and compliance

By examining these indicators, lenders gain a clearer picture of how a business operates and how stable its revenues are over time. When combined with other financial signals such as bank transactions and payment activity, GST data can help lenders form a more complete view of a borrower’s financial health.

For SMEs that maintain regular GST compliance but lack formal credit history, this data can become a strong indicator of creditworthiness.

Cash Flow-Based Lending for SMEs

Another important shift in digital lending is the growing adoption of cash flow-based loan models in India.

Traditional lending focuses heavily on assets and balance sheets. Cash flow-based lending, on the other hand, evaluates how money moves through a business.

Instead of focusing only on collateral, lenders examine questions such as:

- How stable are the business’s monthly revenues?

- Are supplier payments consistent?

- Does the business maintain healthy working capital cycles?

AI systems analyse transaction-level data to identify patterns in income and expenditure. This allows lenders to assess repayment capacity based on actual business performance rather than static financial statements.

For growing SMEs, this approach can be particularly beneficial because it reflects their current operating strength rather than their historical borrowing record.

Business Loans Without CIBIL Score: A Growing Reality

As lending models evolve, it is increasingly possible for businesses to access funding even when they have limited or weak bureau histories.

In many cases, lenders can approve a business loan without a CIBIL score by evaluating a combination of:

- GST returns

- Bank cash flows

- Digital transaction data

- Business activity patterns

AI-based credit models combine these inputs to generate composite risk assessments that may be more predictive than bureau scores alone for new-to-credit borrowers.

This approach is gradually expanding access to credit for small businesses that previously struggled to qualify for formal financing.

Infrastructure Enabling the Shift

Several developments in the financial ecosystem are accelerating the adoption of AI-driven lending.

Digital data-sharing frameworks now allow borrowers to share verified financial information with lenders through secure, consent-based systems. These frameworks enable institutions to access bank statements, investment data, and financial records digitally without manual document submission.

Initiatives such as the Unified Lending Interface (ULI) are also being explored to create open, API-based infrastructure that simplifies how lenders access borrower data and deliver credit services.

Combined with advances in data analytics and cloud-based lending platforms, these developments are making credit decisioning faster and more reliable.

What This Means for the Future of Business Lending

AI-powered credit decisioning is not replacing traditional credit evaluation entirely. Instead, it is expanding the set of tools available to lenders.

Credit bureau scores will continue to play an important role, but they are increasingly becoming just one component in a broader risk assessment framework.

For SMEs, this shift has significant implications. Businesses that maintain strong operational discipline, steady revenue flows, and good compliance records can demonstrate creditworthiness even without an extensive borrowing history.

For lenders, the benefits are equally clear:

- Faster loan processing

- Better risk assessment

- Access to a larger borrower base

- Lower underwriting costs

As digital financial data becomes more accessible, the lending industry will continue moving toward more data-driven and contextual decision-making models.

Capital should accelerate growth, not slow it down

Conclusion

The lending landscape is undergoing a quiet transformation. Instead of relying solely on static credit bureau scores, lenders are increasingly adopting AI credit decisioning India frameworks that incorporate real-time business data.

By combining alternative credit scoring, GST-based analysis, and cash flow evaluation, financial institutions can assess borrower risk more accurately and extend credit to previously underserved businesses.

For SMEs, this means that access to funding is gradually becoming less dependent on historical credit records and more aligned with actual business performance.

As AI underwriting systems continue to evolve, the possibility of securing a business loan without a CIBIL score is no longer an exception. It is becoming a natural outcome of a more data-rich and technology-driven lending ecosystem.

In this evolving landscape, platforms like OPEN Capital help simplify access to credit by connecting businesses with lending partners and streamlining the loan discovery process. For growing SMEs, such platforms make it easier to explore suitable funding options based on their business needs and financial profile.

Frequently Asked Questions (FAQs)

1. How is AI used in credit decisioning?

AI is used in credit decisioning to analyse large volumes of financial data and identify patterns that indicate a borrower’s creditworthiness. These systems can evaluate signals such as transaction history, GST filings, payment behaviour, and cash flow trends. This helps lenders assess risk more efficiently and support faster credit evaluation and approval processes.

2. Can a business get a loan without a CIBIL score?

In some cases, businesses may still be able to access financing even with limited credit history. Lenders may evaluate alternative financial signals such as GST returns, bank transactions, and business cash flows to assess the financial health of the business. These data points can help determine creditworthiness, especially for businesses that are new to formal borrowing.

3. What is alternative credit scoring?

Alternative credit scoring is an approach that evaluates borrowers using non-traditional financial data instead of relying only on credit bureau records. Lenders may analyse information such as digital payments, bank transaction history, utility bill payments, and tax filings. This provides a broader view of a borrower’s financial behaviour.

4. What is cash flow–based lending for SMEs?

Cash flow–based lending assesses a business’s ability to repay a loan based on its ongoing revenue and transaction activity. Instead of focusing primarily on collateral or past borrowing history, lenders analyse patterns in income, expenses, and working capital cycles. This approach is particularly useful for growing SMEs with limited credit history.