When businesses extend credit, payments don’t always happen instantly. To make such transactions legally secure, formal financial instruments are used. Two of the most common are promissory notes and bills of exchange.

If you’ve searched for the difference between promissory note and bill of exchange, you’re likely trying to understand how they work, how many parties are involved, and which one suits your transaction. While both are negotiable instruments used in credit transactions, they differ in their structure, legal obligations, and practical uses.

In this guide, we’ll explain their meaning, features, differences, and when to use each—clearly and practically.

What is a Promissory Note?

A promissory note is a written promise made by one person (the maker) to another (the payee) to pay a certain amount of money at a future date or on demand.

It’s a simple instrument that formalises a credit agreement—without the need for third-party involvement. Promissory notes are widely used when one party lends money to another, either in a personal or business context.

Download Free Promisory Note Template →

Key features of a promissory note:

- Two parties involved: The person who promises to pay (maker) and the one who receives the payment (payee).

- Unconditional promise: The maker agrees to pay a fixed sum without conditions.

- Written and signed: It must be in writing and signed by the maker.

- Specific amount and date: Clearly mentions the amount and the date of payment.

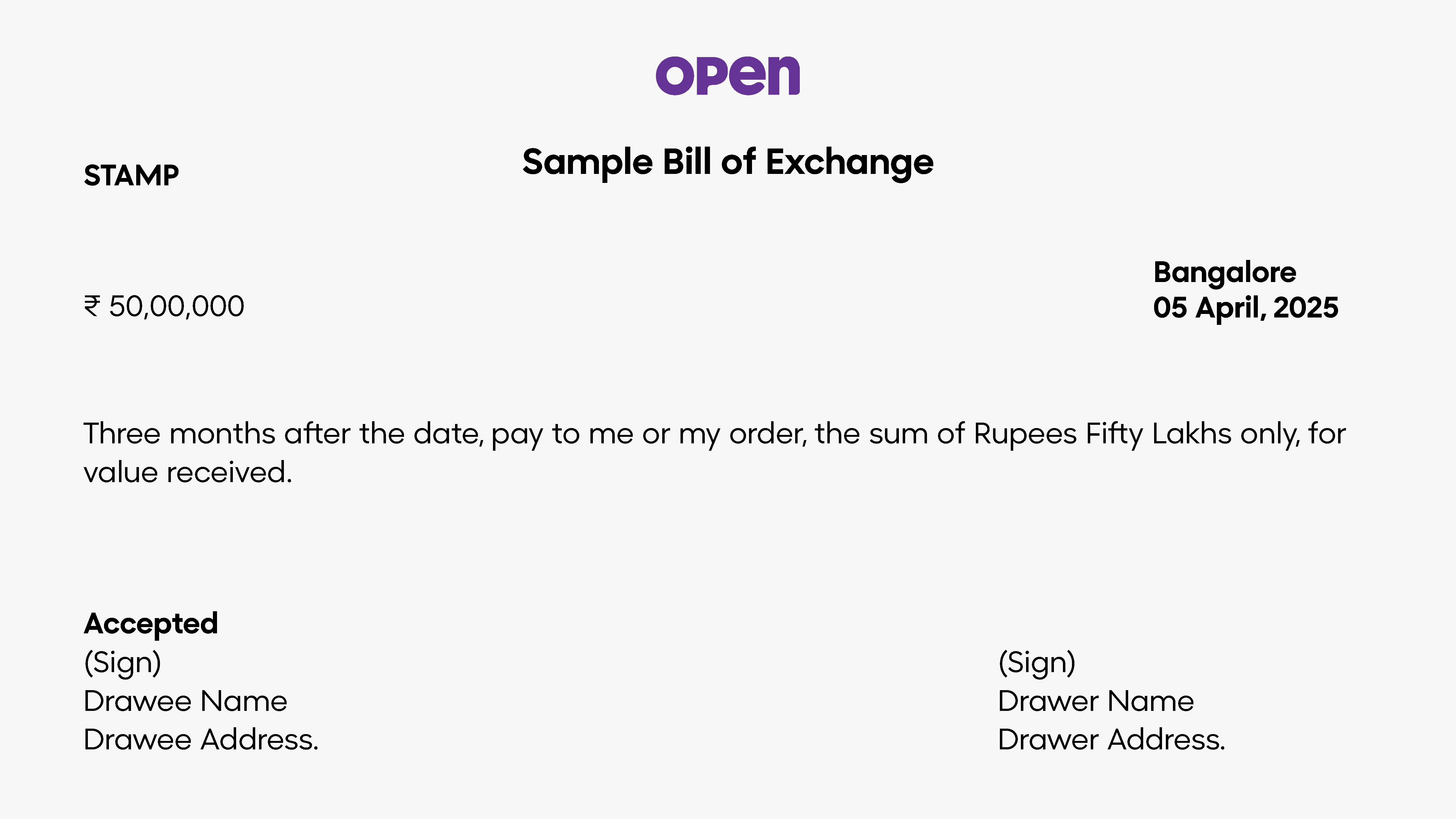

What is a Bill of Exchange?

A bill of exchange is a written order from one person (the drawer) to another (the drawee) to pay a specific amount to a third person (the payee) at a fixed time.

Bills of exchange are commonly used in trade, especially when goods are sold on credit. Unlike promissory notes, they involve three parties and usually require acceptance by the drawee to be valid.

Key features of a bill of exchange:

- Three parties involved: Drawer (who makes the bill), drawee (who pays), and payee (who receives the money).

- Order to pay: It’s an instruction—not a promise—to pay a certain amount.

- Needs acceptance: The drawee must accept the bill by signing it.

- Often used in trade: Especially useful in credit sales or exports.

Difference Between Promissory Note and Bill of Exchange

Here’s a quick comparison to help you understand the difference between a promissory note and a bill of exchange:

| Point of difference | Promissory note | Bill of exchange |

| Parties involved | Two (maker and payee) | Three (drawer, drawee, and payee) |

| Nature | Promise to pay | Order to pay |

| Acceptance required | No | Yes, the drawee must accept |

| Issued by | Debtor | Creditor |

| Use case | Personal loans, business credit | Trade transactions, credit sales |

| Legal standing | Legal proof of debt | Legal direction for payment |

| Transferability | Can be transferred | Can be endorsed and transferred |

When to Use What?

Choosing between a promissory note and a bill of exchange depends on the nature of your transaction.

- If you’re lending money directly and need a legal assurance of repayment, a promissory note is appropriate. It’s straightforward and doesn’t require a third party’s acceptance.

- If you’re selling goods or services on credit and want the buyer to accept liability for payment, a bill of exchange offers more security. It allows for clear direction, endorsement, and transferability if needed.

In business, bills of exchange are particularly helpful for managing receivables. Since they can be endorsed to others, they also serve as negotiable instruments, useful for settling other dues. Bills of exchange are also commonly used in international trade for secure cross-border transactions.

Both promissory notes and bills of exchange are governed under the Negotiable Instruments Act, 1881 (India), which provides the legal framework ensuring their enforceability and protecting the rights of the parties involved.

Final Thoughts

Both promissory notes and bills of exchange play important roles in credit-based transactions. They help create trust and provide legal backing in the event of payment disputes. Understanding the difference between bill of exchange vs promissory note ensures that you’re using the right instrument to protect your interests and maintain smooth financial operations.

Whether you’re lending, buying, or selling on credit, it’s always a good idea to formalise the terms clearly and in writing. If you’re dealing with high-value or frequent transactions, consult with your legal or finance team to ensure compliance and enforceability.

Frequently Asked Questions (FAQs)

1. What is the difference between a promissory note and a bill of exchange?

A promissory note is a written promise by the debtor to pay a certain amount to the creditor. It involves two parties and does not require acceptance.

A bill of exchange is a written order issued by the creditor directing the debtor to pay a specific amount. It involves three parties and must be accepted by the drawee.

2. How many parties are involved in a bill of exchange?

A bill of exchange involves three parties:

- Drawer (who creates the bill)

- Drawee (who must pay)

- Payee (who receives payment)

3. Is acceptance required for a promissory note?

No. A promissory note does not require acceptance because the maker directly promises to pay.

However, a bill of exchange must be accepted by the drawee to become legally enforceable.